Now Reading: How Kenya Raised an Astonishing $1.04 Billion Startup Funding in 2025 – the Highest in Africa’s History

-

01

How Kenya Raised an Astonishing $1.04 Billion Startup Funding in 2025 – the Highest in Africa’s History

How Kenya Raised an Astonishing $1.04 Billion Startup Funding in 2025 – the Highest in Africa’s History

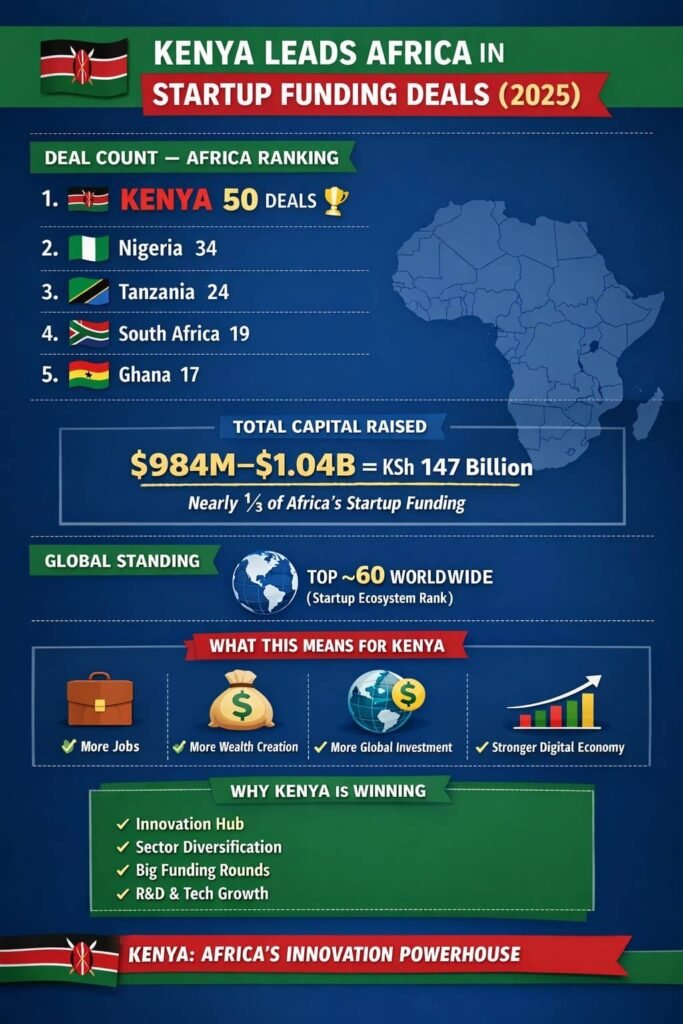

Kenyan startups raised an unprecedented $1.04 billion in 2025, the largest amount of capital ever secured by a single African market in a single year, cementing the country’s position as the continent’s premier inovation hub.

Kenya accounted for nearly one-third of all startup capital raised across Africa in 2025, placing it ahead of traditional funding heavyweights such as Egypt, South Africa, and Nigeria.

Across the continent, startups collectively raised about $4.1 billion in equity and debt financing, marking a 25 percent increase compared with 2024 and signaling a recovery after two years of subdued venture investment.

60% Came as Debt

Data shows that about 60 percent of the capital raised by Kenyan startups in 2025 came in the form of debt, amounting to roughly $582 million, while equity investment totaled approximately $383 million.

This was overwhelmingly driven by large financings into mature, asset-heavy clean energy and consumer credit companies with predictable cash flows and bankable receivables.

Four megadeals alone accounted for approximately $610 million, 60% of Kenya’s total:

d.light expanded its receivables financing facility by $300 million, the largest single transaction in Kenya’s pipeline. The facility bundles future payments from customers buying solar kits on installment, using them as collateral to access capital upfront. This is consumer finance infrastructure, not venture equity.

Sun King closed a $156 million securitization deal in July, structured by Citi and backed by a consortium including Stanbic Bank Kenya, KCB Bank, Absa, and Co-operative Bank, the largest commercial-bank-backed securitization of its kind in Sub-Saharan Africa outside South Africa.

M-KOPA continued raising through a mix of debt and equity, maintaining its position as one of East Africa’s most consistently funded companies.

Burn Manufacturing and PowerGen added to the clean energy concentration reinforcing the clean energy pattern.

The Untold Story of struggling early-stage startups

Despite the record funding total, the number of Kenyan startups securing investment actually declined.

While total capital surged for established firms, the number of Kenyan fresh ventures raising at least $100,000 fell 23 percent year-on-year to just 75 companies, the steepest decline among Africa’s four largest startup markets.

The shift suggests investors are becoming more selective, favoring companies with proven revenue models and strong operational scale rather than early-stage startups.

Industry observers describe the trend as a “flight to quality,” where investors prioritize mature businesses capable of generating predictable returns.

Also, Kenya’s fintech sector, once the country’s dominant driver, saw equity funding sharply decline, attracting just 13 percent of the country’s equity compared to over 40 percent in previous years.

Similarly, the seed-to-Series A conversion rate tells a troubling story: only 5 percent of seed-funded Kenyan startups successfully raised a Series A, roughly 85 percent below the global average.

The facts show that a small number of scaled, bankable companies are accessing large volumes of non-dilutive capital, while the broader ecosystem beneath them is thinning out, maening that starting a business in Kenya coud still be challenging.

Expanding early-stage venture capital, supporting Series A funding rounds, and nurturing startups outside Nairobi are obvious priorities for gaining and sustaining momentum.

Nevertheless, Kenya’s 2025 performance confirms its position as one of Africa’s most influential innovation economies, where technology, finance, and energy solutions are increasingly attracting global investment.

How Kenya Stacked Up Against the Continent

Across Africa, startups raised $3.2 billion in 2025, a 40 percent increase from 2024 and the first annual rise after two consecutive years of contraction.

Investment remained heavily concentrated in Africa’s four dominant markets. Kenya, Egypt, Nigeria, and South Africa attracted 82 percent of all startup funding, a proportion largely unchanged since 2019.

Egypt followed closely with $614 million, also up 51 percent from 2024, split roughly evenly between equity and debt. The country emerged as the second-largest destination for debt financing on the continent.

South Africa ranked third with $600 million, growing 51 percent year-over-year. Unlike Kenya, the market was overwhelmingly equity-driven, with more than 90 percent of capital raised through equity rounds.

South Africa also recorded a sharp rise in deal activity, with 83 ventures raising at least $100,000, up 63 percent from the previous year.

Nigeria underperformed its peers, raising $343 million, down 17 percent from the previous year. Its share of total African startup funding fell to 11 percent, the lowest level recorded since 2019.

Despite the drop, Nigeria remained the continent’s most active market by deal count, with 86 ventures raising at least $100,000, highlighting a shift toward smaller rounds and reduced investor risk appetite.

Outside the Big Four, only two countries recorded more than $100 million in startup funding. Senegal rose to fifth place with $157 million, largely due to a single large debt round by fintech Wave, while Benin ranked sixth after Spiro raised $100 million.

Sector Shifts: Beyond Fintech

Fintech remained Africa’s largest funded sector in 2025, raising $769 million in equity, 25 percent of total equity investment. However, its share continued to decline as other industries gained traction.

Cleantech recorded $550 million in funding, a 186 percent increase year-on-year. Healthtech attracted $215 million, up 232 percent. Enterprise-focused startups raised $238 million, representing a 55 percent increase.

For the first time since 2021 and 2022, several non-fintech sectors each surpassed $200 million in annual equity funding, signaling a more diversified and mature ecosystem.

Clean Energy Takes the Lead

Clean energy emerged as one of the biggest beneficiaries of the funding surge.

Kenya’s renewable energy landscape, where more than 90 percent of electricity is generated from renewable sources, has helped create a supportive regulatory and infrastructure environment for energy startups.

Companies offering solar home systems, electric cooking solutions and distributed energy products have attracted large amounts of financing as investors increasingly view them as infrastructure-like businesses rather than traditional startups.

The strong pipeline of financing in this sector reflects Kenya’s broader ambition to become a regional leader in green energy and climate technology innovation.

Previous Post

Next Post