Now Reading: Africa’s Mobile Money Surge Reveals Regional Strategy Gaps

-

01

Africa’s Mobile Money Surge Reveals Regional Strategy Gaps

Africa’s Mobile Money Surge Reveals Regional Strategy Gaps

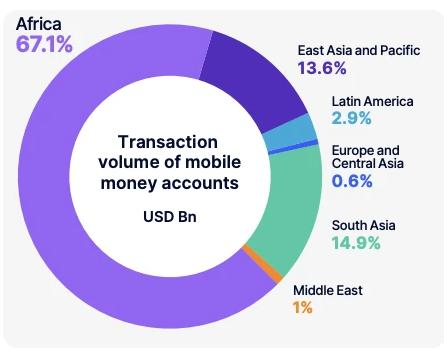

Africa’s mobile money growth has reached a defining milestone, with over $1.4 trillion processed across the continent in the past year—accounting for nearly two-thirds of global mobile money transactions. Yet beneath this headline figure lies a far more complex reality. The growth is heavily concentrated in just two regions, East and West Africa, which together account for roughly 92% of total activity. This uneven distribution highlights a critical insight for investors, fintech operators, and policymakers: Africa is not a single mobile money market, but a collection of distinct ecosystems shaped by different economic structures, regulatory environments, and user behaviors.

As mobile money growth continues to accelerate in Africa, understanding these regional dynamics is becoming essential for unlocking value. What works in one market may fail entirely in another, making localized strategy a prerequisite for success in the continent’s rapidly evolving fintech landscape.

Africa’s Mobile Money Growth Driven by East and West Africa Dominance

East Africa remains the undisputed leader in Africa’s mobile money growth, processing more than $800 billion across approximately 61 billion transactions. The region’s defining characteristic is scale combined with low transaction values, averaging around $13 per transfer. This reflects the deep integration of mobile money into everyday life, where it functions as core financial infrastructure for payments, remittances, and daily commerce. Countries like Kenya have pioneered this model, embedding mobile money into nearly every aspect of economic activity.

West Africa, by contrast, stands out for its diversity and competitiveness. With around $500 billion processed and 76 live mobile money services, the region represents the most dynamic and fragmented market on the continent. Ghana has emerged as a standout performer, combining high per capita usage with one of the most advanced regulatory environments globally, according to the GSMA. Meanwhile, Nigeria is undergoing a rapid transformation. Historically a laggard in mobile money adoption, Nigeria has seen transaction volumes surge by over 1,500% since 2021, driven by fintech platforms such as OPay, PalmPay, and Paga. This shift signals the emergence of a new growth frontier within the region.

Structural Differences Shape Africa’s Mobile Money Growth Across Regions

Beyond East and West Africa, the remaining regions present markedly different profiles that further illustrate the complexity of mobile money growth in Africa. In North Africa, total transaction value remains relatively low at around $15 billion, but the average transaction size is the highest on the continent. This indicates a more niche use case, where mobile money is used for higher-value, less frequent transfers rather than daily transactions.

Central Africa represents a high-growth, early-stage market where infrastructure is still being developed. While volumes remain modest, the region offers significant upside potential as mobile networks expand and financial inclusion improves. For investors, this “emerging market within an emerging market” presents opportunities to establish early positions in underserved ecosystems.

You Might Also Like: Africa Stablecoin Payments Hit $5B as ZendWallet Redefines Global Trade

Southern Africa, particularly South Africa, presents a unique paradox. Despite having one of the most advanced banking sectors on the continent, mobile money adoption remains relatively low. The presence of established financial institutions and widespread access to traditional banking services has reduced the need for mobile money solutions, highlighting how financial maturity can influence adoption patterns.

As Africa’s mobile money growth continues to evolve, the key takeaway is clear: there is no universal strategy for success. Market characteristics—ranging from regulatory frameworks to consumer behavior—must guide decision-making at every level. For fintech companies, investors, and solution providers, the ability to adapt to these nuances will determine whether they capture meaningful market share or miss the opportunity entirely.

The next phase of Africa’s digital payments revolution will not be defined by scale alone, but by precision. Understanding each market on its own terms—its infrastructure, its users, and its economic realities—will be the difference between sustainable growth and strategic missteps in one of the world’s most dynamic fintech landscapes.

Related Posts

Previous Post

Next Post