Now Reading: The Shilling Stabilization Story — Is It Sustainable?

-

01

The Shilling Stabilization Story — Is It Sustainable?

At one point in 2023 and early 2024, the Kenyan shilling weakened beyond KSh 160 against the US dollar, raising alarm across markets. Import costs surged, fuel prices climbed, and inflationary pressures intensified. Businesses struggled to price goods accurately, while households absorbed higher costs in food and transport.

Since then, the currency has regained relative stability. The exchange rate has hovered at steadier levels, restoring a measure of confidence. However, stabilization alone does not answer the central question: is this recovery durable, or merely cyclical?

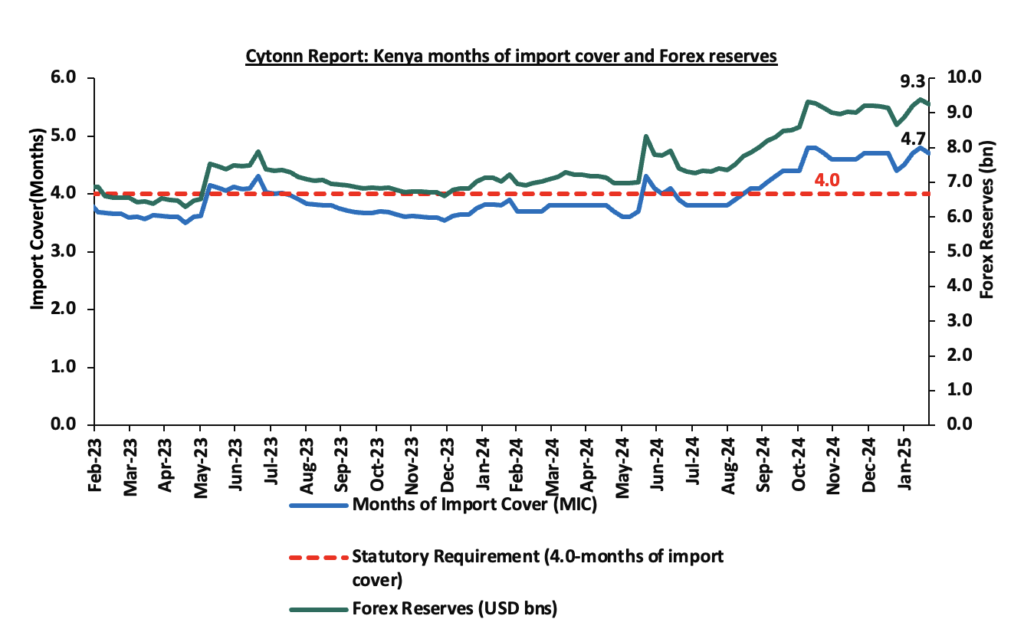

The Reserve Cushion

The Central Bank of Kenya has maintained foreign exchange reserves equivalent to roughly four to five months of import cover in recent periods. This buffer plays a critical role in defending the currency against speculative attacks and smoothing volatility. Stronger reserves reassure investors and signal capacity to meet external obligations.

Yet reserves depend on continued inflows and disciplined outflows. If global commodity prices spike or external financing tightens, the cushion can erode quickly. Stability built solely on reserve defense is rarely permanent without structural support.

Remittances and External Lifelines

Diaspora remittances have consistently exceeded $4 billion annually, making them one of Kenya’s largest sources of foreign exchange. These flows provide a steady stream of dollar liquidity, supporting both household consumption and currency stability.

However, remittances depend on economic conditions abroad. A slowdown in the United States or Europe could reduce inflows, weakening the balance of payments. Relying heavily on external lifelines exposes the currency to shocks beyond domestic control.

Debt and the Dollar Burden

Kenya’s external debt obligations remain substantial, particularly those denominated in dollars. When the shilling depreciates, debt servicing costs rise in local currency terms. Stabilization reduces immediate pressure, but underlying debt levels remain.

Fiscal consolidation efforts and refinancing strategies have helped ease short-term stress. Nevertheless, sustainability requires careful borrowing discipline. A stronger currency cannot permanently offset structural debt accumulation.

Trade Balance Realities

Kenya’s exports remain concentrated in tea, horticulture, tourism, and a narrow band of goods. Meanwhile, imports include petroleum, machinery, vehicles, pharmaceuticals, and industrial inputs. The structural trade deficit continues to weigh on the currency.

Sustainable stability demands export diversification and value addition. Without narrowing the gap between imports and exports, exchange rate calm may prove temporary. Currency markets respond not only to policy signals, but to trade fundamentals.

Inflation and Policy Trade-Offs

Monetary tightening helped curb inflationary pressures during the depreciation phase. Higher interest rates stabilized demand and supported the currency. Inflation has moderated compared to peak volatility periods.

However, elevated rates can constrain private sector borrowing and investment. Policymakers face a delicate balance between defending the currency and sustaining growth. Stability achieved at the expense of economic dynamism is difficult to maintain.

A Test of Fundamentals

Currency markets reward consistency and discipline. If Kenya maintains strong reserves, manages debt prudently, diversifies exports, and preserves investor confidence, the shilling’s stabilization could hold. If structural imbalances persist, pressure may resurface.

The recent calm is encouraging, but it is not definitive. Exchange rate sustainability ultimately depends on productivity, fiscal discipline, and export strength. The shilling’s future will be shaped less by short-term defense and more by long-term reform.

Stability, therefore, is not a destination. It is a reflection of economic fundamentals. The question is whether those fundamentals are strengthening fast enough to anchor the currency through the next global shock.

Also Read: Kenya’s Middle Class Is Shrinking — And We’re Pretending It Isn’t

Previous Post

Next Post